On February 20, 2026, the Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that President Trump’s tariffs imposed under IEEPA (International Emergency Economic Powers Act) were unlawful. The core holding: IEEPA’s authorization to “regulate importation” does not include the power to impose tariffs. Over $160 billion in tariff refunds and a fundamental reshuffling of U.S. trade policy are now in motion.

The ruling is clear. But when you cross-reference the majority opinion with Kavanaugh’s 63-page dissent, structural cracks in Roberts’ reasoning emerge — cracks that are hard to ignore. This piece maps the ruling, then dissects those four cracks.

The Ruling: Why IEEPA Tariffs Were Struck Down

What IEEPA Actually Says

IEEPA, enacted in 1977, authorizes the President to “regulate importation” of foreign property during a declared national emergency. The Trump administration invoked this provision as the legal basis for the “Liberation Day” tariffs of April 2025, the fentanyl-related tariffs on Canada, Mexico, and China, and the country-specific reciprocal tariffs that followed.

The legal question was narrow: IEEPA never mentions the words “tariff” or “duty.” Does “regulate importation” mean “impose tariffs”? That was the only question before the Court.

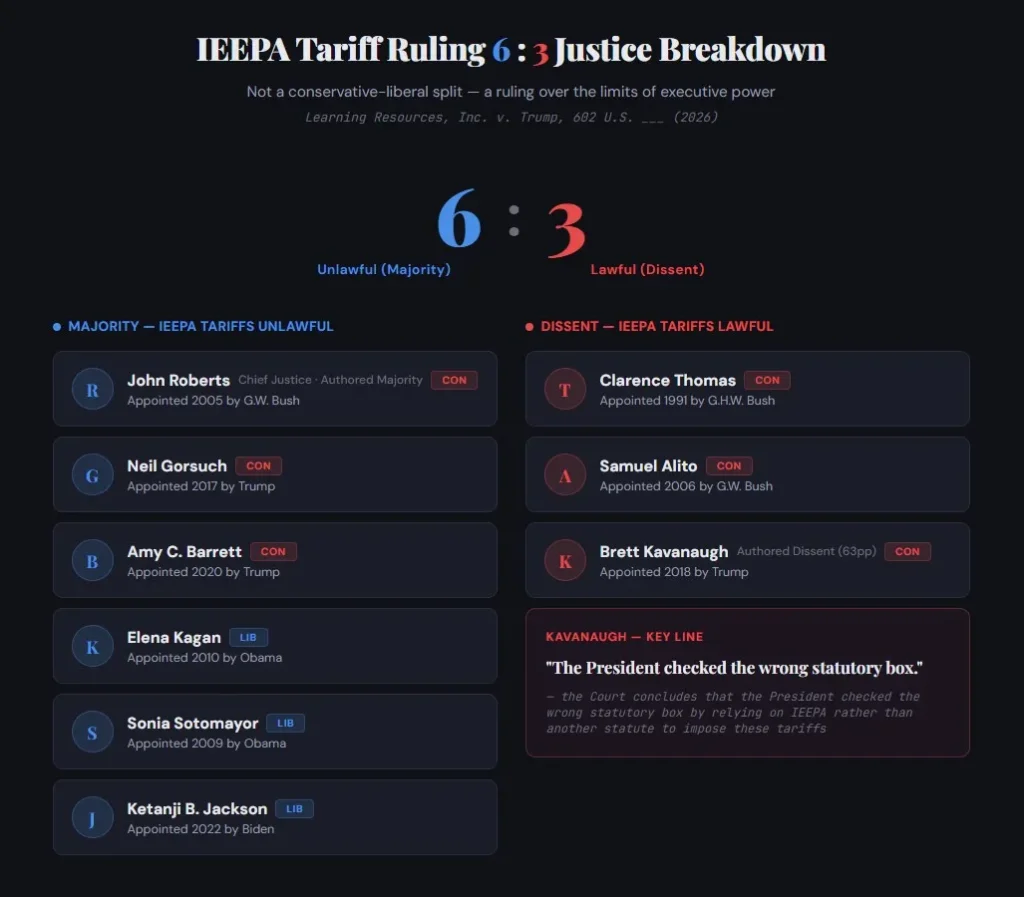

A Peculiar 6-3 Split

What struck me first about this ruling was the vote alignment. On the majority side: Roberts, Gorsuch, and Barrett from the conservative wing, joined by Kagan, Sotomayor, and Jackson from the liberal wing. In dissent: Thomas, Alito, and Kavanaugh. This was not a conservative-liberal split — it was a split over the limits of executive power. The fact that Gorsuch and Barrett — both Trump appointees — voted against Trump’s signature policy underscores the constitutional weight of this decision.

What’s equally notable is the fracture within the majority itself. The Roberts-Gorsuch-Barrett trio applied the Major Questions Doctrine, reasoning that Congress would not have delegated something as consequential as unlimited tariff authority through an ambiguous statutory term. The Kagan-Sotomayor-Jackson trio agreed on the outcome but explicitly rejected the Major Questions Doctrine, arguing that IEEPA’s text alone was sufficient to exclude tariffs. Six Justices agreed on the result. They disagreed on why.

The Majority’s Three-Step Argument

Roberts’ majority opinion follows a clear three-step structure.

Step one — the constitutional premise. Article I, Section 8 of the Constitution vests in Congress the power “to lay and collect Taxes, Duties, Imposts, and Excises.” Roberts cited Gibbons v. Ogden (1824) to confirm that the tariff power is “very clearly a branch of the taxing power.” The Founders, he wrote, “did not vest any part of the taxing power in the Executive Branch.”

Step two — textual analysis. IEEPA authorizes the President to “investigate, block during the pendency of an investigation, regulate, direct and compel, nullify, void, prevent, or prohibit” transactions involving foreign property. That’s a long list. “Tariff” and “tax” are nowhere in it. Roberts noted that “the government could not identify a single statute in which ‘regulate’ authority has been construed to include ‘tax’ authority.”

Step three — the Major Questions Doctrine. This was the reasoning of the Roberts-Gorsuch-Barrett trio alone. The principle holds that when an agency claims authority over a question of “vast economic and political significance,” it must point to clear congressional authorization. IEEPA’s vague “regulate” language fails that test.

Kavanaugh’s Dissent: The Core Question

One sentence from Kavanaugh’s dissent captures the essence of this ruling better than anything in the majority opinion: “In essence, the Court today concludes that the President checked the wrong statutory box.”

What I found most compelling in the dissent was the simplicity of Kavanaugh’s counter-argument. Both sides agreed that IEEPA authorizes the President to impose quotas (import limits) and embargoes (total import bans). If quotas and embargoes qualify as “regulating importation,” why don’t tariffs? A President who can ban 100% of imports cannot impose a $1 tariff — that, Kavanaugh argued, is incoherent.

Kavanaugh also presented historical precedent. In 1971, President Nixon used TWEA (Trading with the Enemy Act) — IEEPA’s predecessor statute — with the identical “regulate importation” language to impose a 10% global tariff. The Court of Customs and Patent Appeals upheld it. When Congress drafted IEEPA in 1977, it knew about the Nixon precedent and adopted the same language. If Congress intended to exclude tariffs, Kavanaugh argued, it had every opportunity to say so — and didn’t.

Four Logical Flaws in the Majority Opinion

Cross-referencing the majority opinion with the dissent, I identified four structural weaknesses in Roberts’ reasoning.

Flaw 1: Conflating “Includes” with “Equals” — Does Revenue Make It a Tax?

Roberts’ central argument is that tariffs are “a branch of the taxing power” and therefore can only be imposed by Congress. This rests on the fact that tariffs generate revenue. But “generates revenue” and “is a tax” are not the same thing.

Regulatory actions that incidentally generate revenue are everywhere. Fines generate revenue but are not taxes. Licensing fees generate revenue but are not taxes. Tariffs can function as a tool to “regulate” import flows while incidentally generating revenue. As Kavanaugh noted, the primary function of a tariff is to alter the flow of imports, not to raise revenue.

Solicitor General Sauer made this argument during oral argument, calling the revenue effect of tariffs “incidental and collateral.” This came in response to Roberts pressing him on whether tariffs that “substantially reduced our deficit” were effectively domestic tax collection. In my reading, the “regulatory tariff vs. revenue tariff” distinction was the strongest argument in the government’s arsenal — one that should have been pressed more forcefully from the lower courts onward.

Flaw 2: Roberts Contradicts Himself — 2012 vs. 2026

This is the sharpest point. Reading this ruling, I couldn’t avoid the conclusion that Roberts is in direct tension with a decision he himself authored 14 years ago.

In NFIB v. Sebelius (2012) — the Obamacare case — Roberts “saved” the individual mandate by recharacterizing it as a “tax.” The core logic: the mandate imposes a financial burden on people who don’t buy insurance, but that burden is avoidable — just buy insurance. An “avoidable financial burden,” Roberts reasoned, is a tax, not a penalty. Substance over form.

In Learning Resources v. Trump (2026), Roberts classified tariffs as “a branch of the taxing power” and struck them down. But tariffs share the exact same structural characteristic as the mandate — they are avoidable. Import domestic goods, and you pay zero tariffs. In 2012, Roberts called an “avoidable financial burden” a tax to save it. In 2026, he called an “avoidable financial burden” a tax to kill it. Form over substance.

The 2012 Roberts said “look at the substance.” The 2026 Roberts said “look at the form.” Same Chief Justice, same logical structure, opposite conclusions.

Flaw 3: Avoidability Undermines the “Tax” Frame

This extends directly from Flaw 2. Tariffs are fundamentally avoidable. If an American consumer or importer chooses a domestic alternative, they pay nothing.

This is not “compulsory extraction of money” (the essence of taxation) — it’s an “incentive structure designed to alter behavior” (regulation). And this is precisely the mechanism through which tariffs achieve their regulatory purpose: promoting domestic production, reducing import dependence. When a tariff “succeeds,” revenue actually declines. Can you call a mechanism whose revenue shrinks as its purpose is achieved a “tax”?

In 2012, Roberts said “avoidable, therefore still a tax.” In 2026, Roberts again said “avoidable, still a tax.” But the conclusions pointed in opposite directions — one saved a law, the other struck one down.

Flaw 4: The “Pretext” Concern Is Abstract — Tariffs Are Always Concrete

Roberts worried that reading “regulate” to include tariffs would let the President impose “unlimited tariffs” under the pretext of a national emergency. But this concern is abstract.

Every tariff is imposed on a specific HTS (Harmonized Tariff Schedule) code, against a specific country, at a specific rate. 25% on Chinese semiconductors. 20% on Canadian lumber. These are objectively verifiable administrative actions. The worry that “a President could use emergency declarations as a pretext for taxation” is a different question entirely from “does a 25% tariff on Chinese semiconductors constitute import regulation in response to a national security emergency?”

As Kavanaugh pointed out, the Court chose to answer the abstract question — can IEEPA ever authorize tariffs — rather than the concrete one — were these specific tariffs a valid exercise of emergency import regulation. This is a departure from judicial restraint.

What This Ruling Actually Means

For the post-ruling trade landscape — Trump’s alternative authorities, the 150-day clock, country-by-country impact — see After the IEEPA Ruling: Trump’s Tariff Alternatives and the 150-Day Clock.

Here, I’ll focus on the legal legacy.

First, the President’s tariff toolbox has shrunk. IEEPA provided “anywhere, anything, any rate, any time” flexibility. The alternative authorities — Sections 122, 232, 301, 338 — each come with constraints: time limits, rate caps, investigation requirements, or country-specific targeting mandates.

Second, the Major Questions Doctrine has expanded into trade. Previously applied mainly to domestic regulation (environmental, health), the Doctrine now covers foreign affairs and trade policy. As Roberts put it, “there is no Major Questions exception to the Major Questions Doctrine.”

Third, the refund question is unresolved. Over $160 billion in IEEPA tariffs have been declared unlawful, but the Court remanded refund mechanics to the lower courts. As Kavanaugh warned, this process could become a “mess.” Trump has signaled he has no plans to issue refunds since the Court didn’t directly order them, and litigation will likely continue for years.

Fourth, this is not the end of tariffs. Kavanaugh’s diagnosis is the most accurate: “The President checked the wrong statutory box.” He didn’t lose the ability to impose tariffs — he lost his most flexible tool. Trump signing a Section 122-based global tariff within hours of the ruling proves the point.

FAQ — Frequently Asked Questions

No. Only IEEPA-based tariffs were struck down. Section 232 tariffs (25% on steel, aluminum, autos, etc.) and Section 301 tariffs (up to 25% on Chinese goods) remain in full effect. Per Tax Foundation estimates, Section 232 tariffs alone represent $635 billion over the next decade and an average $400 per U.S. household burden in 2026.

Legally, yes — the tariffs were unlawful from inception. However, the Court remanded refund procedures to the Court of International Trade, meaning individual importers may need to file petitions or join existing litigation. Tax Foundation estimates over $160 billion in cumulative IEEPA tariff collections; Penn Wharton pegs the refund-eligible amount at approximately $175 billion. Notably, DOJ made a judicial estoppel commitment during lower court proceedings that it would not argue liquidation prevents refunds.

On the same day, he signed an executive order imposing a 10% global tariff under Section 122 of the Trade Act of 1974. The following day, he raised it to 15% — the statutory maximum. The tariff took effect February 24, with a 150-day limit expiring July 24, 2026. He also announced new Section 301 and Section 232 investigations and stated he has no plans for refunds since “the Court didn’t even discuss it.”

IEEPA-based tariffs on Korean goods are voided, but the Section 122 global tariff of 15% replaces them. Section 232 tariffs on autos (25%) remain unchanged. A Section 232 investigation on semiconductors is ongoing, which directly affects Samsung and SK Hynix. Korean exporters should immediately review their IEEPA tariff payment records for potential refund claims.

Sources

Learning Resources, Inc. v. Trump, 602 U.S. ___ (2026) — Full Opinion

Tax Foundation, “Supreme Court Trump Tariffs Ruling: Analysis” (Feb. 20, 2026)

Council on Foreign Relations, “How Trump’s Tariffs Could Survive the Supreme Court Ruling” (Feb. 20, 2026)

CFR, “After the Supreme Court Ruling, What Is Next for Trump’s Tariffs?” (Feb. 20, 2026)

SCOTUSblog, “Watching tariffs come down” (Feb. 20, 2026)

Brownstein, “Supreme Court Restricts Presidential Tariff Authority Under IEEPA” (Feb. 20, 2026)

Flexport, “The Supreme Court’s IEEPA Tariff Ruling: Next Steps” (Feb. 20, 2026)